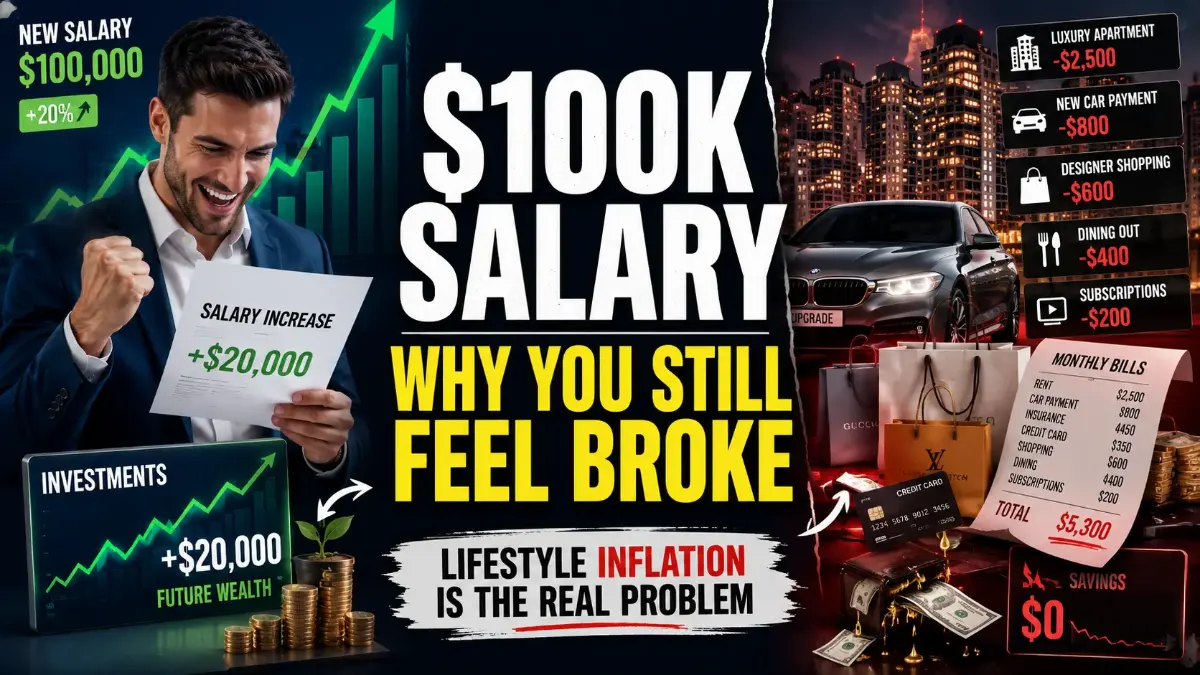

Imagine getting a promotion at work.

Your salary jumps from $70,000 to $90,000.

You tell yourself you'll save more.

Invest more.

Build wealth faster.

Yet six months later, your bank account looks exactly the same.

Sound familiar?

You're not alone.

Millions of people experience this every year, and there's a name for it:

Lifestyle inflation.

It's one of the biggest reasons people struggle to build wealth despite earning good incomes.

In many cases, it's not low income that keeps people broke.

It's rising spending.

What Is Lifestyle Inflation?

Lifestyle inflation occurs when your spending increases as your income increases.

Instead of using extra income to save or invest, you gradually upgrade your lifestyle.

It usually happens slowly.

You get a raise.

You move into a nicer apartment.

You upgrade your car.

You start dining out more often.

You buy more expensive clothes.

You travel more.

None of these purchases seem unreasonable on their own.

The problem is that they become permanent expenses.

Over time, every raise disappears.

Why Lifestyle Inflation Is So Dangerous

The biggest danger is that it feels normal.

Most people don't wake up one morning and decide to double their spending.

Instead, they make small upgrades over several years.

Consider two people earning $120,000 annually.

Person A increases spending every time income rises.

Person B keeps expenses relatively stable and invests the difference.

After ten years, their financial situations could look completely different despite earning similar incomes.

This is why some people earning six figures still struggle financially while others quietly build wealth.

The Modern Lifestyle Inflation Trap

Lifestyle inflation has become easier than ever.

Social media constantly exposes people to lifestyles that appear normal but are actually expensive.

Luxury vacations.

Designer clothing.

High-end apartments.

New cars.

Expensive restaurants.

People compare themselves to others and gradually increase spending to keep up.

The result is a cycle where income rises but financial freedom never arrives.

Signs You May Be Experiencing Lifestyle Inflation

Many people don't realize it's happening.

Here are some common warning signs.

Your Savings Rate Never Improves

Your income increases, but your savings account doesn't.

Every Raise Disappears

Within a few months, extra income is fully absorbed by new expenses.

You Feel Broke Despite Earning More

This is one of the strongest indicators.

You Frequently Upgrade Everything

Phone.

Car.

Apartment.

Subscriptions.

Vacations.

Each upgrade adds ongoing costs.

How Lifestyle Inflation Destroys Wealth

The real cost isn't today's spending.

It's the future value of money not invested.

Imagine spending an extra $500 every month because of lifestyle upgrades.

That's $6,000 per year.

Invested over decades, that money could potentially grow into a significant retirement asset.

Many people underestimate how powerful consistent investing can become.

That's one reason reaching milestones like How Long Does It Take to Save Your First $100,000? often takes longer than expected.

Income growth helps.

But keeping more of that income matters even more.

Why High Earners Are Especially Vulnerable

Many people assume lifestyle inflation only affects middle-income households.

In reality, high earners often face the biggest risk.

A larger income creates more opportunities to spend.

This explains why some individuals earning $250,000 or more still experience financial stress.

Earning a high salary doesn't automatically create wealth.

As discussed in What Salary Is Considered Rich in America in 2026?, income and wealth are not the same thing.

One is what you earn.

The other is what you keep.

Lifestyle Inflation vs Real Quality Of Life

Not all spending increases are bad.

Some upgrades genuinely improve life.

Moving closer to work.

Improving healthcare.

Creating a safer living environment.

Investing in education.

These can be worthwhile.

The goal isn't to avoid spending entirely.

The goal is to spend intentionally rather than automatically.

How Wealthy People Think Differently

Many wealthy individuals focus on assets before lifestyle.

When income rises, they often allocate money toward:

- Investments

- Businesses

- Real estate

- Retirement accounts

- Emergency funds

Only after those priorities are addressed do they increase lifestyle spending.

This approach helps explain why net worth often matters more than salary.

The difference becomes clear when examining What Net Worth Makes You Upper Middle Class in 2026?.

How To Avoid Lifestyle Inflation

Automate Saving First

Increase savings automatically whenever income increases.

Follow The 50% Rule

When receiving a raise, save or invest at least half of the increase.

Focus On Net Worth

Track assets rather than income alone.

Delay Major Upgrades

Wait several months before making expensive purchases.

Avoid Comparison Spending

Most people only see the highlights of other people's lives.

Not their debt.

Not their financial stress.

The Connection To Retirement

Lifestyle inflation doesn't just affect monthly budgets.

It can dramatically impact retirement outcomes.

The more your lifestyle expands, the more money you'll eventually need to retire comfortably.

Someone spending $60,000 annually requires far less retirement savings than someone spending $150,000.

This is why controlling spending remains one of the most powerful retirement strategies.

It's closely connected to questions explored in How Much Money Do You Need to Retire Comfortably in 2026?.

The Bottom Line

Lifestyle inflation is one of the most common reasons people fail to build wealth.

It doesn't happen overnight.

It happens one upgrade at a time.

A nicer apartment.

A more expensive car.

A bigger monthly payment.

A few extra subscriptions.

Individually, these choices seem harmless.

Together, they can consume years of future wealth.

The people who build lasting financial security are not always those who earn the most.

Often, they are the people who learn how to keep more of what they earn.