Every generation believes it faces unique financial challenges. Millennials often point to the housing affordability crisis and the scars left by the 2008 financial meltdown. Gen Z argues they entered adulthood during a period of record inflation, soaring rents, and economic uncertainty.

But when it comes to building wealth, which generation is actually doing better?

The answer depends entirely on how you define success.

If the goal is total wealth accumulated, Millennials are comfortably ahead. They own more homes, hold larger retirement accounts, and have spent more years climbing career ladders.

If the goal is wealth-building momentum, however, Gen Z is moving at a remarkably fast pace. Despite having far less money today, younger workers are accumulating assets faster than Millennials did when they were the same age.

In other words, Millennials are winning the race on distance traveled, while Gen Z may be running the faster lap.

The Wealth Gap by the Numbers

One of the most important distinctions in wealth analysis is the difference between average and median net worth.

Average figures can be distorted by a relatively small number of ultra-wealthy households. Median figures, by contrast, represent the midpoint of the population and provide a more realistic picture of the typical person's financial position.

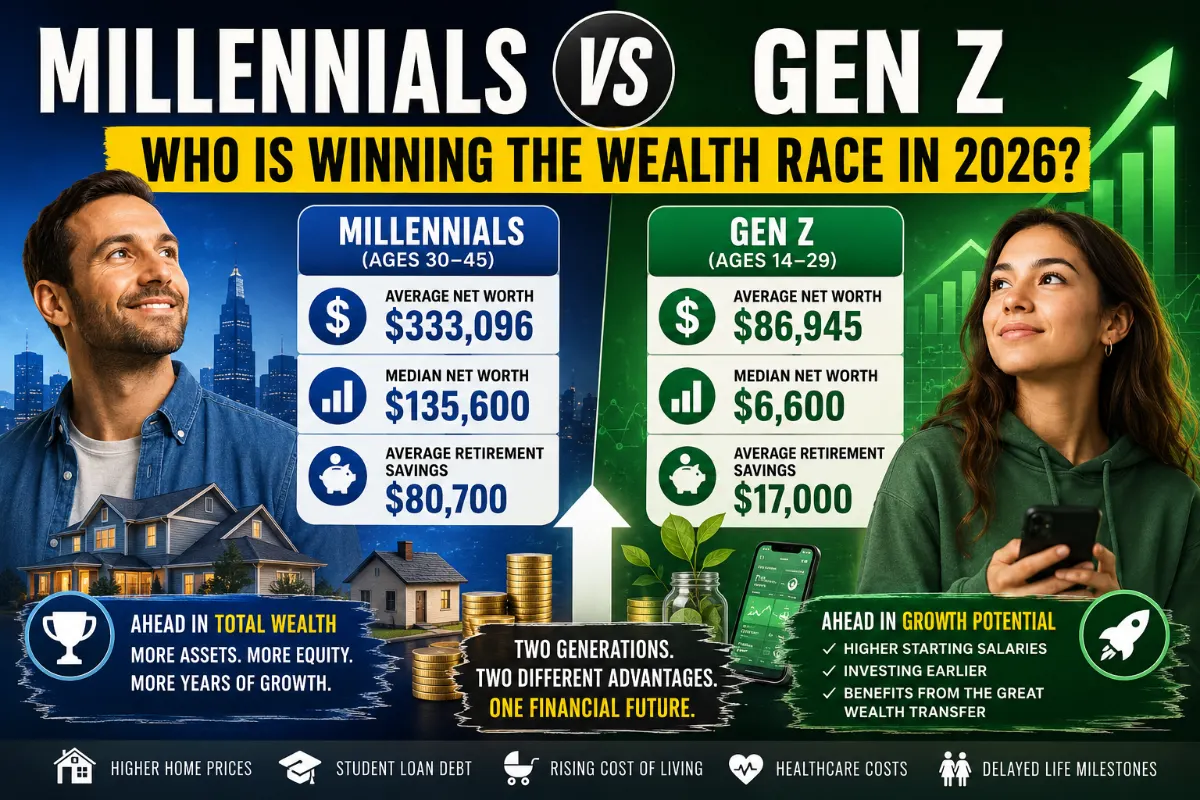

Millennials (Ages 30–45)

Average net worth: $333,096

Median net worth: $135,600

Average retirement savings: $80,700

Gen Z (Ages 14–29)

Average net worth: $86,945

Median net worth: $6,600

Average retirement savings: $17,000

At first glance, the results appear decisive.

Millennials possess significantly more wealth across virtually every major category. They have accumulated larger retirement balances, more investment assets, and substantially more home equity.

However, that comparison only tells part of the story.

Millennials have had an additional decade or more to build wealth.

The more revealing question is how quickly each generation is progressing relative to where they started. Individuals curious about their own financial standing can benchmark their progress using Virearn's net worth calculator

Why Millennials Lead in Total Wealth

Millennials currently occupy what economists often call the "wealth accumulation sweet spot."

Many are in their peak earning years, earning promotions, managing businesses, and maximizing retirement contributions.

The biggest factor behind their wealth advantage is real estate.

A significant portion of Millennials purchased homes before mortgage rates surged and before housing prices reached today's levels.

As home values appreciated throughout the late 2010s and early 2020s, homeowners accumulated substantial equity without necessarily making additional investments.

For many households, homeownership became their single largest source of wealth creation.

This timing advantage is difficult to overstate.

A Millennial who purchased a home before the sharp rise in housing costs often benefited from both lower purchase prices and historically low mortgage rates. The affordability challenges facing younger buyers today can be seen clearly in the New York City housing market outlook for 2026, where inventory shortages continue to push prices higher.

Gen Z largely missed that window.

As a result, younger buyers face much steeper barriers to entry into the housing market.

Why Gen Z Is Building Wealth Faster

While Millennials currently hold more wealth, Gen Z appears to be accumulating assets at a faster rate than previous generations did at similar ages.

Several factors are driving this trend.

Higher Starting Salaries

Unlike Millennials, who entered the workforce during or shortly after the Great Recession, many members of Gen Z began their careers in an unusually strong labor market.

Competition for talent pushed wages higher, particularly in technology, healthcare, engineering, and skilled trades.

Higher starting salaries provide a stronger foundation for saving and investing early.

Earlier Exposure to Investing

Previous generations often viewed investing as something people began doing later in life.

Gen Z has largely rejected that approach.

Many young adults opened brokerage accounts while still in college or shortly after graduation. Fractional-share investing, commission-free trading, and financial education through social media have dramatically lowered the barriers to entry.

As a result, more young investors are benefiting from compound growth earlier than previous generations.

Even small investments made in one's early twenties can produce substantial long-term gains. This mindset aligns closely with principles discussed in how the ultra-wealthy use the Core-and-Satellite strategy to balance long-term growth with risk management.

The Great Wealth Transfer

Perhaps the most significant long-term catalyst is the ongoing transfer of wealth from older generations.

Economists estimate that tens of trillions of dollars are expected to pass from Baby Boomers to younger generations over the coming decades.

This transfer includes:

Investment portfolios

Retirement assets

Real estate

Family businesses

Cash inheritances

Because Gen Z is positioned to receive assets from both grandparents and parents over time, many analysts expect the generation's wealth trajectory to accelerate significantly during the next two decades.

For some households, inheritance will become a major component of future net worth growth.

The Uneven Reality of Wealth

While generational comparisons are useful, they can sometimes hide substantial differences within each generation.

Not all Millennials are thriving.

Not all Gen Z workers are rapidly building wealth.

Economic data consistently shows that wealth accumulation remains highly uneven across income groups, educational backgrounds, and demographic categories.

One of the most persistent challenges is the racial wealth gap.

Historical differences in homeownership rates, inherited wealth, student debt burdens, and access to capital have created substantial disparities in household wealth accumulation.

These differences often compound across generations, making wealth-building opportunities far from equal.

As a result, average generational statistics rarely tell the entire story.

The Challenge Both Generations Share

Despite their differences, Millennials and Gen Z face a common obstacle.

The cost of adulthood has become dramatically more expensive.

Housing costs remain elevated.

Childcare expenses continue to rise.

Healthcare costs consume larger portions of household budgets.

Student debt remains a burden for millions.

These pressures have forced many young adults to postpone major life milestones.

Across both generations, large numbers of people report delaying:

Homeownership

Marriage

Parenthood

Entrepreneurship

Long-term financial commitments

In many cases, the delay is not driven by changing preferences but by economic necessity.

The financial threshold required to feel secure has moved significantly higher than it was for previous generations. Rising living expenses are one reason why many households increasingly rely on tools such as a cost of living calculator to better understand how location affects their financial goals.

So, Who Is Really Winning?

The answer depends on the metric.

If success is measured by total wealth, Millennials are clearly ahead.

They own more assets, have larger retirement accounts, and benefit from years of home equity accumulation.

If success is measured by growth rate and future potential, Gen Z appears to have the advantage.

They are investing earlier, entering higher-paying labor markets, and stand to benefit from one of the largest wealth transfers in history.

Perhaps the most accurate conclusion is that both generations are winning different parts of the race.

Millennials currently hold the lead because they started earlier.

Gen Z may have the stronger acceleration.

The final outcome will depend on factors that extend beyond salaries and investment returns—including housing affordability, economic growth, inheritance patterns, and public policy.

The Bottom Line

Comparing Millennials and Gen Z is not simply a battle between two generations. It is a reflection of how economic conditions shape wealth creation.

Millennials built wealth through career progression and a fortunate housing market window.

Gen Z is leveraging technology, earlier investing habits, and a stronger early-career labor market to accelerate wealth accumulation.

Today's younger workers also have access to educational resources and digital income opportunities that barely existed a decade ago, including the emergence of AI-powered freelancing and digital work platform

Today, Millennials remain wealthier.

Tomorrow, Gen Z may narrow that gap faster than many expect.

The real lesson is that wealth is not built overnight. Whether you're a Millennial or Gen Z, the most powerful drivers of financial success remain remarkably consistent: earning more, saving consistently, investing early, and allowing time to do its work.

Generations may differ, but the mathematics of wealth creation rarely change.